In a big win for consumers facing ever-growing health care cost burdens, the Board of the Office of Health Care Affordability voted today to set a 3% health care cost growth spending target over five years, with a phase-in starting at 3.5% in 2025. SACRAMENTO, CA – After a long debate, the board of California’s […]

Office of Health Care Affordability Takes Major Action to Rein in Health Care Spending

In Continued Solidarity with the Labor Movement, Health Access is Now a Union Employer

As an organization that has long fought for patients’ and workers’ rights in coalition with the labor movement, Health Access is proud to announce that we are now a union employer! In a historic move for the organization, Health Access has voluntarily recognized its first staff union, Health Advocates United – UAW local 2013. This […]

AB 3129 (Wood) Putting Patients Over Profits: Oversight on Private Equity and Hedge Fund Health Care Takeovers

Background Health care costs are outpacing inflation, taking bigger and bigger chunks out of Californians’ incomes and wages. More than half of Californians say they skip or delay care due to high costs. A major driver of these rising costs are health care mergers. As health systems and other health care corporations get bigger, they […]

Advocates Rally at the State Capitol in Support of #Health4All Covered California

Tuesday, April 9, 2024 Media Contacts: Rachel Linn Gish, Health Access California Communications Director, rlinngish@health-access.org Ed Sifuentes, CIPC Communications Director, esifuentes@caimmigrant.org SACRAMENTO – The #Health4All coalition rallied yesterday at the State Capitol for a more inclusive, universal health care system for ALL Californians, regardless of immigration status. While historic gains have been made in removing […]

Longtime Leader of California’s Health Consumer Advocacy Coalition Tapped to Lead National Counterpart, Families USA

As Executive Director of Health Access California for 22 years, Anthony Wright led the organization to win dozens of health reforms, coverage expansions, patient protections, public health investments, cost containment efforts and more, including the biggest drop of the uninsured rate of all 50 states following the passage of the Affordable Care Act. SACRAMENTO, CA […]

SB 1061 (Limón) Removing Medical Debt from Credit Reports

More than one in three Californians have medical debt . . . When someone has unaffordable medical expenses those unpaid bills often turn into medical debt that is included on their credit report. This damages their credit score and may affect their ability to get an affordable car loan or a mortgage, to rent an […]

Legislators and Advocates Unveil 2024 Care4all California Bills for Health Reform

Thirteen CA proposals announced today to get California to a more universal, accessible, and equitable health system, as soon as possible SACRAMENTO, CA – Today health care advocates gathered with legislative champions at the State Capitol to highlight important health reform bills in the 2024 legislative session. The thirteen bills and budget items featured as […]

CA State Assembly Passes Patient Protection to Ensure Accurate Plan Provider Directories

AB 236 (Holden), which seeks to improve the accuracy of health plan provider directories for consumers, now heads to the California Senate. ***Impacted consumer stories available upon request*** SACRAMENTO, CA – Today, the California State Assembly passed AB 236 by Assemblymember Chris Holden, which will ensure accurate health plan provider directories, and help consumers […]

New Office of Health Care Affordability Proposal Would Limit Health Cost Growth, Offering Real Relief to Californians

Health and consumer advocates praise new staff recommendations of the Office of Health Care Affordability to set a statewide health growth target at 3% OHCA’s Health Care Affordability Board to make final decision in coming months SACRAMENTO, CA – California’s ambitious effort to rein in the skyrocketing cost of care enters a new phase this […]

AB 4 (Arambula) Accessing Coverage in Covered California

Undocumented Californians are explicitly and unjustly excluded from accessing and purchasing health care coverage plans through Covered California, the state’s marketplace established under the federal Affordable Care Act (ACA). Assembly Bill 4 (Arambula), the #Health4All Covered California campaign, would address this exclusion by taking the first step toward allowing undocumented Californians to buy health plans […]

AB 4 (Arambula) Acceso a la cobertura médica con Covered California

Los californianos indocumentados están explícita e injustamente excluidos del acceso y la compra de planes de cobertura de salud a través de Covered California, el mercado del estado establecido bajo la Ley Federal de Cuidado de Salud Asequible (ACA). El proyecto de ley de la Asamblea 4 (Arambula) abordaría esta exclusión dando el primer paso […]

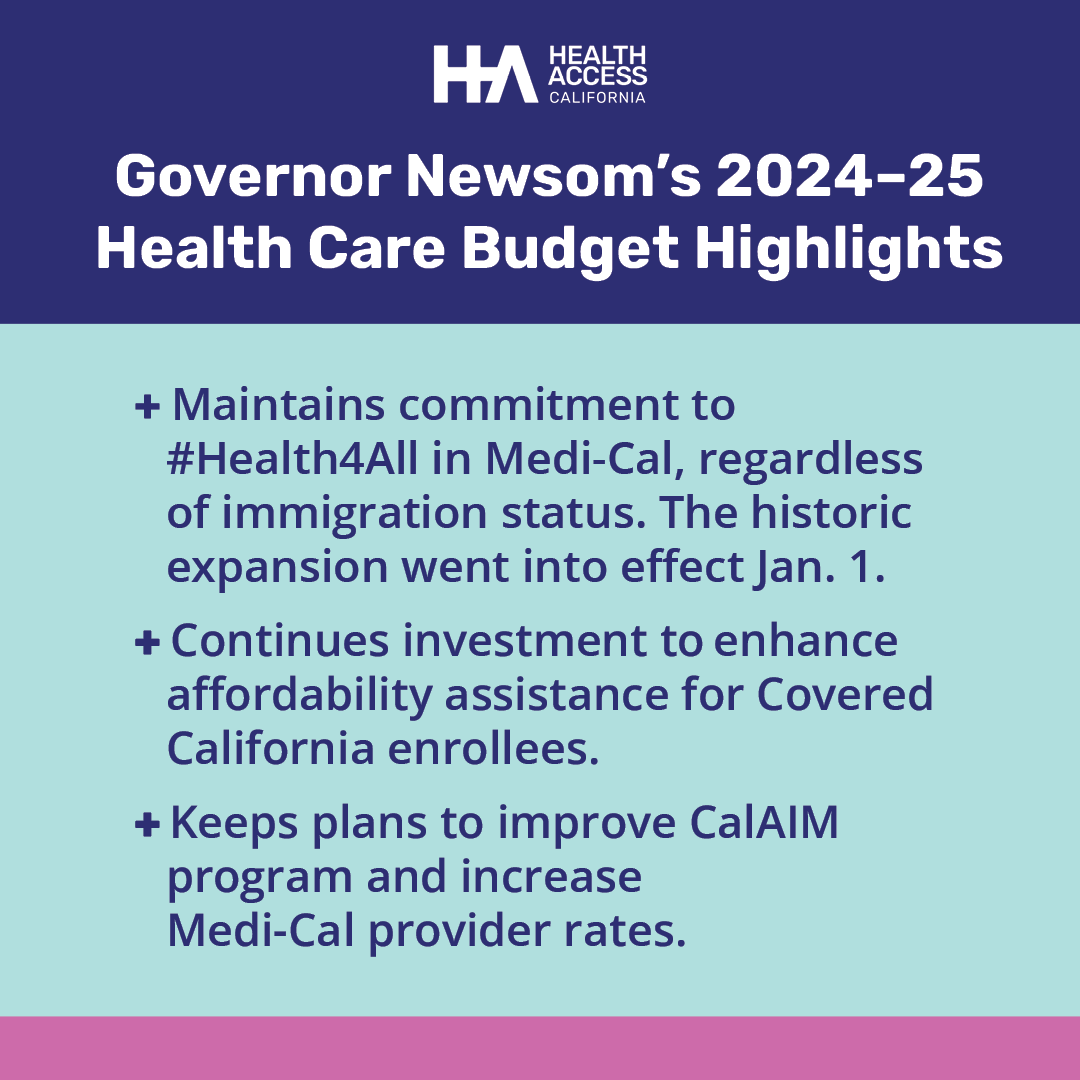

Governor Newsom’s 2024-25 Budget Continues California’s Key Commitments in Health Care

Despite a deficit, the 2024-2025 state budget proposed by Governor Gavin Newsom continues key commitments in health care, particularly in Medi-Cal with improvements in rates and access, benefits, quality and equity, and eligibility, and keeping Medi-Cal available for all income-eligible Californians regardless of age or immigration status. As Californians face rising cost-of-living pressures, and higher […]

AB 236 (Holden) Ensuring Accurate Health Plan Provider Directories

BREAKING: #AB236 (@chrisholdennews) passed out of the #CAStateAssembly with 46 votes, and now it’s headed to the #CAStateSenate! 🎉 https://t.co/WL7lUMLkIc — Health Access CA (@healthaccess) January 30, 2024 Background Every health plan in California is required to maintain an updated list of in-network health care providers for their enrollees. These directories list providers such […]

2023 in Review

In 2023, Health Access advocated to provide real relief and remove financial barriers to California health consumers—successfully helping increase access to and/or reduce the cost of coverage, care, prescription drugs, and even ground ambulance services. We supported major investments in Medi-Cal to improve access and continue the commitment to expand coverage to all those who […]

Premiums Remain Low and New Reductions in Deductibles and Co-pays

Today marks the start of the 11th open enrollment period of Covered California and the most affordable year ever for enrollees, with new, significant state and federal financial assistance available. The Inflation Reduction Act continues major premium assistance for the nearly 2 million Californians in Covered California through 2025. Funding included in this year’s state […]

Bill Signed by Governor Newsom to Permanently Cap Prescription Drug Costs

AB 948 (Berman) keeps expensive prescription drugs more affordable for Californians with chronic illnesses SACRAMENTO, CA – Over the weekend, California Governor Gavin Newsom has signed AB 948 by Assemblymember Berman to make permanent the existing $250 co-pay cap for prescription drugs, ensuring consumers can count on their monthly prescription drug costs staying consistent, even […]

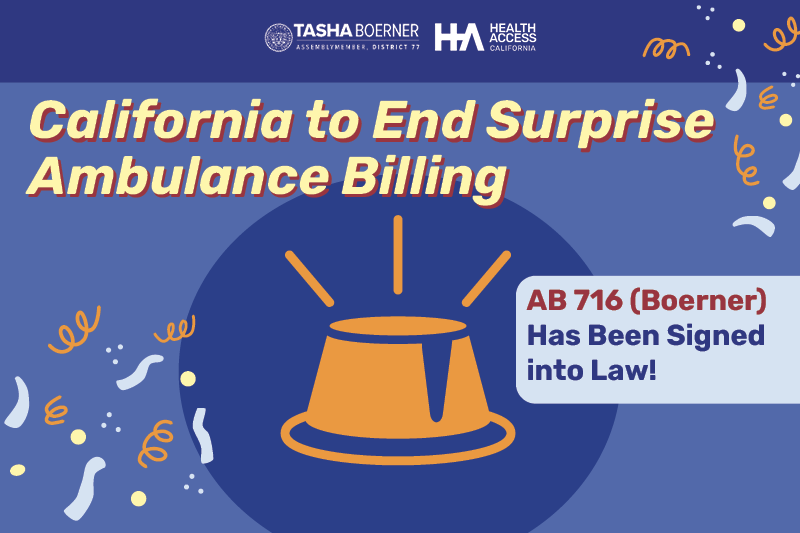

CA Governor Gavin Newsom Signs Bill to End Surprise Ambulance Billing for Californians

One of the most impactful health consumer bills this year, AB 716 (Boerner) will prevent Californians from getting $1,000 plus surprise ambulance bills, and take consumers out of the middle of ambulance billing disputes ***Impacted consumer stories available upon request*** SACRAMENTO, CA – Today California Governor Gavin Newsom has signed AB 716 by Assemblymember Tasha […]

Health Access Joins New National Coalition: Consumers for Fair Hospital Pricing

Health Access California is proud to be a part of a new national coalition of health consumer advocates that are taking on skyrocketing hospital costs as a main driver of our growingly unaffordable health system. Consumers for Fair Hospital Pricing is about standing up to the big hospitals that have become big business, and fighting […]

State Senate Passes AB 716 to End Surprise Ambulance Billing for Californians

One of the most impactful health consumer bills currently before the CA state legislature, AB 716 (Boerner) takes Californians out of the middle of ambulance billing disputes ***Impacted consumer stories available upon request*** SACRAMENTO, CA – Yesterday with unanimous bipartisan support, California’s State Senate passed AB 716 by Assemblymember Tasha Boerner to end a major […]

We’re Close to Stopping Surprise Ambulance Bills!

We’ve been fighting all year, and now our effort to stop surprise ambulance bills is close to the finish line. We need your help right now to get it done. Use our easy tool to tell your State Senator to vote YES to stop surprise ambulance bills! At this crucial moment, we need you to […]

Page 1 of 33